Wither on the vine? The unfulfilled EU Single Market for Services

Liberalization of services in the EU has lost steam. Compared to the Single Market for goods, trade in services remains tethered to an adolescent stage, resulting in slower growth, lower employment and subpar competitiveness.

- Download the report

- Executive summary

- Introduction

- Obstacles amplified and competitiveness

- World Bank Doing Business captures red tape levied on both domestic and non-domesticbusinesses

- Explicit trade obstacles

- Restrictions on professional services

- Lacking the clarity of ‘one obstacle to rule them all’?

- Summary and conclusions

- Läs rapporten på svenska

The obstacles to trade in services are as diverse as the services themselves. By combining different indices, this report presents a macro picture of regulatory obstacles. Based on OECD data, there are specific sectors (such as legal, distribution and rail freight transport services) where reform should be possible at little cost to governments. But red tape and bureaucracy challenge all businesses in the EU. More than 90 percent of EU GDP stems from countries that rank lower than 20 in the 2020 World Bank’s Doing Business assessment.

Notably, about 140 non-medical professions are regulated in one EU country only (such as florists in Luxembourg and wine tasters in Slovenia.

The more than 5,700 regulated professions in the EU are another area ripe for reform. Notably, about 140 non-medical professions are regulated in one EU country only (such as florists in Luxembourg and wine tasters in Slovenia). There are also curious regional differences in regulating professions within countries (especially in Belgium). The many regulated professions thwart the full potential of the Single Market; they could be reduced and harmonized with political will. If only professions common to a reasonably large number of EU countries (say twenty) were subject to regulation, the list of such professions would shrink dramatically.

This report concludes that the cost of inaction on service liberalization is high and risks EU competitiveness.

The Single Market has increased economic growth and contributed to job creation across the EU. Without it, EU countries would be poorer than they are. But a core question remains: to what extent do red tape and regulation keep the Single Market from fulfilling its potential? Some regulation is necessary to uphold safety and trust.

Still, there can be too much of a good thing – especially when the mechanisms for creating new rules are more vigorous than those for pruning anachronist ones. As time passes, old regulations accumulate while their original motivations grow obsolete, and their benefits are outweighed by their detrimental effects on growth and innovation. The extent to which this is happening in the EU is far from an academic question, as member countries struggle to gain competitiveness vis-à-vis Asian and North American economies.

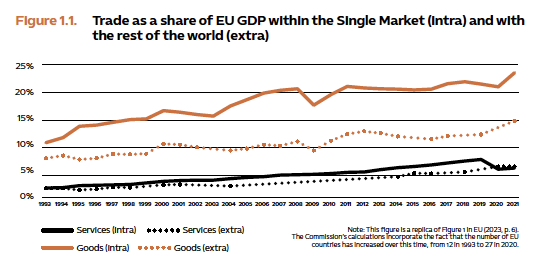

While trade in goods has expanded significantly since 1993, when the Single Market was created, trade in services remains tethered to an adolescent stage (see Figure 1.1). As a share of EU GDP, trade in goods has increased from about 11 percent in 1993 to 23 percent in 2021.2 By contrast, trade in services has increased only modestly, from about 3 percent in 1993 to about 6 percent in 2021. Even considering the somewhat higher pre-pandemic level of trade in services (8 percent in 2019), this increase of 3 percentage points is lacklustre compared to the 11 percentage point increase for trade in goods over the same period. On one estimate, the Single Market has only reduced trade costs in services by about 7 percent, compared to 20 percent for goods.

Figure 1.1. Trade as a share of EU GDP within the Single Market (intra) and with the rest of the world (extra)

According to one calculation, such restrictions cost the EU asmany a 705,000 jobs per year, depleting some professions by asmuch as 9 percent in some places

This subpar performance for trade in services is further highlighted by the contrasts between intra- and extra-EU trade in goods and services, as can also be seen in Figure 1.1. In 2021, trade in services with countries outside the EU represented about the same share of EU GDP, while the gap in goods between intra-EU and extra-EU trade was almost 9 percentage points. This indicates that trade frictions for goods inside the Single Market are an order of magnitude lower than those for services. In addition, intra-EU trade in services should be much higher than extra-EU trade, and that gap should be expanding. Instead, for thirty years intra- and extra-EU trade in services have grown in lockstep, as if glued together, and only by a few percentage points.

This report argues that the regulatory hurdles for intra-EU trade in services remain onerous, especially for small and medium size companies. Copenhagen Economics, a consultancy firm, has argued that full implementation of the Service Directive could add some 2 percent to the EU GDP.4 But the effects could be more significant if the Service Directive’s coverage were expanded and archaic regulations were eliminated. The Directive currently covers less than half of

the EU GDP, while services comprise about 70 percent. Careful review and assessment of the Directive with the aim of further liberalisation would strengthen the Single Market and increase economic growth.

The obstacles are multi-dimensional. Regulation in the form of requirements on professional qualifications typically imply the need to hold a specific a degree, exam or membership of a professional body. Few would question the need for such regulation in areas such as medicine. But there are many regulated professions in areas where the benefits are unclear and that should be subject to liberalisation. Essentially, the regulated professions create administrative hurdles that hamper the movement of labour and thwart the full benefits of the Single Market.

The regulated professions in the EU are diverse, ranging from crane operators to mountain guides. According to one calculation, such restrictions cost the EU as many a 705,000 jobs per year, depleting some professions by as much as 9 percent in some places.5 Restrictions on exporting services to other EU member states (MS), assessed annually by the OECD’s Services Trade Restrictiveness Index (STRI), clearly decrease trade: a one basis point reduction in STRI can result in a 4 percent increase in trade with services.6 But it is not only country-specific regulations that introduce barriers and costs. Differences between countries make it harder for companies to benefit from economies of scale. In fact, trade restrictions mean that expanding into multiple MS can instead induce significant extra ad valorem equivalent trade costs—by some estimates, 20 to 75% at low levels of the STRI index.

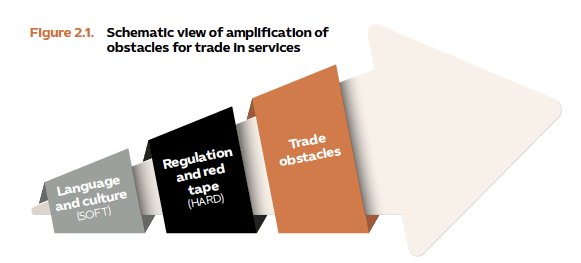

We should view all this holistically. Restrictions on professional qualifications, together with trade obstacles measured by the OECD STRI index, act on businesses that are also reckoning with language and cultural differences between EU countries, and larger economic trends, such as the servification of economies, not least of digital services.8 There is a clear risk that the combined effect of all obstacles is greater than the sum of the parts, not merely adding to the cost of doing business in the EU but multiplying them. Though administrative burdens are levied on all, they are likely to weigh heavier on companies that provide services in several MS and must comply with the idiosyncrasies in each country, thus making it more costly and time-consuming to scale across the EU. As the EU Single Market celebrates its first three decades, it is high time to address these issues. The long-run competitiveness of EU countries depends on overhauling and pruning the Single Market’s regulatory framework.

Red tape and bureaucracy curtail the benefits of scale when exporting services across the EU.

This report is organized as follows. The next section discusses how various regulations are amplified, and the subsequent effects on growth and innovation. The third section discusses the World Bank’s assessments of obstacles in all countries, notably those regulatory hurdles that may be more onerous for non-domestic businesses. The fourth section discusses the OECD measure, STRI, on restrictions of services. The fifth section discusses rules about professional qualifications and the EU mechanism for a single point of contact. The penultimate section uses these different measures to summarize country rankings in obstacles to trade in services. The last section concludes.

Is there an optimal degree of regulation?

Opponents of regulation will sometimes criticize all obstacles for businesses. Maybe they have been captured by the Silicon Valley credo: ‘move fast and break things’. This view is too simplistic. Clearly, very stringent rules that require governmental approval for the most minute matters do stifle growth. However, between the extremes of no regulation and draconian rules, there can exist good (or ‘optimal’) regulation that balances different concerns. Such regulation can help establish standards, both for businesses and households, as well as build trust. Good regulation can create a market and lead businesses to innovate.

Rules that promote green technology are a case in point. By imposing rules on emissions and a price tag on those emissions, governments incentivise private companies to improve their manufacturing processes and to innovate.

To criticise obstacles to trade in services in the EU is not to say that there should be no rules at all, but that there are too many anachronist rules with high cost to growth and employment, as we discuss in this report.

The business case for exporting services to other EU countries

In a 2016 survey, firms reported that the three largest obstacles to trading goods and services in the EU are the following:

- Having to conform to national regulations;

- The remaining regulatory dichotomy between domestic and non-domestic firms;

- The treatment of VAT.

The choice of selling services to other countries in the EU should in principle be based on a calculation of the costs and the benefits of entering those markets. One measure that helps in this regard is the ad valorem equivalent of non-tariff (AVE) calculated, for example, by the World Bank. It is defined as the additional costs associated with the presence of non-tariff barriers. While this is a useful starting point, the measure may not fully capture the time and costs associated with complex regulation. We illustrate this schematically in Figure 2.1.

Let us discuss these in turn.

First, language and cultural differences may have large effects on the type of services available and that are feasible to export. While there

are clear national proclivities in the types of goods that are demanded, the differences are likely to be larger and more heterogenous for services, depending on culture, climate and geography. A case in point is the job of baker/pastry maker, which is regulated in France and 8 other countries but not, for example, in Denmark, Finland or Spain. Since language and cultural differences reflect national identities, they are typically not covered in multilateral harmonisation efforts. Another cultural difference can manifest itself in design choices or preferences. For example, architects tend to draw apartments or houses according to the expectations in that country, which may differ across EU countries. Such soft obstacles may serve to amplify the effects of more tangible barriers and are hard to measure.

Second, some obstacles are levied on all firms, both domestic and non-domestic. On the surface, such rules are non-discriminatory,

as all businesses are required to fulfill them. This may range from how VAT is reported to licensing requirements. In practice, institutional knowledge can bring considerable advantages to domestic firms compared to non-domestic ones in services. One way to address the regulatory burden is to use the World Bank’s Doing Business ranking as a measure of red tape and bureaucracy.

Third, several restrictions explicitly create hurdles for trade in services by non-domestic firms. The OECD has created a methodology to measure such restrictions. Notably, there are vast and inexplicable differences between sectors, which in part stem from the success of special interest lobbying. Heterogeneity in regulation across countries brings in another form of complexity

and increases costs for countries that operate across countries. Another expression of restrictions is the largely unexplainable variety in ways that EU countries treat requirements for professional qualifications. The total effect of all these types of obstacles is likely to be multiplicative rather than additive. For the sake of argument, we could think of each ‘unit’ of difference in language and culture making it that much harder and more time-consuming to overcome various tangible obstacles.

Examples of language/informational hurdles in EU Single Point of Contact

The EU provides a service for a so-called single point of contact to make it easier for firms and individuals to export goods or services to other MS.10 It is a website operated by the ‘EUGO network’ of national coordinators. It provides information to 1) explore business opportunities in other EU countries; 2) requirements to set up businesses abroad; 3) rules that apply; and 4) complete administrative procedures online.

In theory, the website collects links to all countries in the EU and those in the EEA, potentially mitigating the need for businesses to find and navigate domestic websites. In practice, there are vast differences in the kind of information provided and how easy the sites are to navigate. Beyond one or two mouse clicks, webpages may no longer be in English and there are also different rules within countries, depending on region.

Some examples of awkward framing and accessibility of information include:

- For Germany, clicking on the region Rhineland-Palatinate in a map yields an error message and notification ‘page not found’.

- For France, clicks result in a pop-up box with the message ‘Title of browser page in markdown’ (in Safari).

- The page for the Czech Republic quickly lands in text provided only in the Czech language.

More generally, the landing page for each MS may seem functional but the digital information below the landing page tends to be hard to navigate and core material is often available only in the local language. But some EU countries have relatively good websites for the Single Point of Contact, notably: Denmark, Finland, the Netherlands and Sweden.

The EU Service Directive and the professional qualifications directive

The EU Service Directive from 2006 set the foundations for trade in services in the EU.11 Its purpose was to create a Single Market also for services, but not all sectors were included in the initial agreement. Indeed, in the years leading up to the agreement, more fundamental reforms were debated, including the idea of basing trade in services on the country of origin principle. Had this been done, a service approved in one country would also have been approved in other EU countries. This was not to be and a final agreement was watered down compromise and local regulations remaining in place.12 Notably, in Article 2(2) the following exclusions are listed for services:

a. non-economic services of general interest;

b. financial services;

c. electronic communications services and networks;

d. services in the field of transport;

e. services of temporary work agencies;

f. healthcare services;

g. audiovisual services;

h. gambling;

i. exercise of official authority;

j. social services;

k. private security services;

l. services provided by notaries and bailiffs.

There is a variety of reasons for special treatment of these areas and typically, they are covered by other sector-specific directives. Importantly, healthcare is a core welfare area that largely falls outside the scope of EU competence. There is a system of automatic recognition of professional qualifications for health care workers, but the process takes time (more on professional qualifications below). More broadly, the Directive references the concept of ‘overriding reasons relating to the public interest’ that motivates exemptions in areas like air transport.

Perusing the list of excluded areas above, it is possible to conceive of motivations related to the concept of the public interest. But it is also fair to characterize some of the exemptions as rather vague and growing more anachronistic.

Mechanisms to resolve regulatory obstacles

The European Commission and EU countries have implemented a framework to uphold the Service Directive and to address issues. The resulting apparatus provides channels and procedures to remove obstacles inconsistent with EU laws and regulations, but it lacks teeth and is short on enforcement.

There is a well-established mechanism to address trade obstacles inconsistent with regulation in the EU but the procedures lack teeth and venues for enforcement.

The European Commission continues to receive notifications of obstacles. In 2022, for example, DG GROW in the European Commission received almost 200 complaints of malfunctions in the Single Market for assessment, many related to the bad application of EU law.13 There are several mechanisms to remove or alleviate obstacles to trade in services. SOLVIT is a service provided by each MS to which citizens and businesses can address their grievances when, for example, the application of local regulation may be at odds with EU law. While SOLVIT reports having an 85 percent success rate and has resolved about 28,000 cases in the EU over the last 20 years, the process takes time, and not all MS report cases to the system.14 The number of SOLVIT cases has also increased over time.15 It is to be expected that number of cases should rise in the first few years, then stabilize and begin to decline. This has not occurred, and the number of cases now is at about the same level as it was in 2014. More recently, in 2021, the Swedish authority responsible for SOLVIT reported that only about half of its cases were resolved.

It is fair to say that the mechanisms to resolve trade disputes in services are far less forceful than those for goods. There are few direct consequences for a MS that is slow to resolve issues or that does not fulfil its obligations. The Swedish Chamber of Commerce has recommended strengthening SOLVIT by shifting to legally binding rules for compliance and ensuring that national centres are adequately staffed.

Peer pressure has a poor track record in politically charged decisions

Peer pressure is one mechanism in the EU, notably in areas where is no penalty for those MS that deviate from the rules. Perhaps most prominently, the EU Stability and Growth Pact largely relied on peer pressure. In 2000, for example, Germany and France exceeded the rule against deficits larger than 3 percent of GDP (and so did several other countries).18 The peer pressure mechanism did not withstand the perceived political need for fiscal expansion

in those countries. The subsequently revised Stability and Growth Pact relies on a similar aspiration that the peer pressure mechanism induces member states to uphold reforms or keep within agreed budget rules. One example is the EU Macroeconomic Score Board in the Macroeconomic Imbalance Procedure (MIP). After the fallout of the 2007–09 financial crisis, the idea was to identify economic aspects in MS that might indicate an unsustainable path, for example rising private debt. By making it explicit which MS exceeds certain threshold values, the Score Board has improved the conditions for the peer pressure mechanisms to take effect.

Another effort in the EU is the Single Market Enforcement Task Force (SMET) set up in 2020 to strengthen implementation and enforcement of Single Market rules. Its work supplements other enforcement mechanisms. In 2022, the SMET reported concrete results in two areas:

- It removed potentially protectionist measures in the agri-food sector, that supported local production but hampered trade;

- It removed restrictive measures on non-harmonised construction products.

The SMET works to identify obstacles and suggest improvements to the functioning of the Single Market. One fear, however, is that its recommendations are not sufficiently backed by political will. Overall, the extent to which there has been an actual strengthening in enforcement mechanisms is unclear. The experience from the peer pressure mechanism in the MIP is that measures may be toppled by political calculus at home. In the most recent MIP, the number

of EU countries that exceeded the thresholds for public and private debt remained essentially the same over the period 2018–2023.20 Looking ahead, the peer pressure mechanism is likely to remain anaemic and it may even take a turn for the worse. Notably, there has been criticism against Hungary and Poland for eroding EU core ethical standards by subjugating the independence of the judiciary. Compared to such critiques, incomplete implementation of the Single Market, for trade in services in particular, appears decidedly less consequential.

Challenges to competitiveness in Europe

The European Commission routinely publishes various measures related to competitiveness, including unit labour costs, labour productivity, and various measures of exchange rates. In an assessment for 2022, the Commission highlights that:

- Unit labour costs are expected to rise in almost all EU countries, driven by wage compensation that exceeds productivity growth;

- Differing inflation rates in EU countries affect the effective exchange rates;

- EU export market shares in the world economy are expected to fall due to the high energy costs and supply-side disruptions.

These measures are useful to examine the relative changes between Europe and the rest of the world in the short term. But the current relative situation is reflected in many years of accumulated actions that affect the long-run competitiveness of EU countries and businesses. One simple way to capture the long-run impact of competitiveness is to examine how successful businesses have been. Notably, Europe and the United States have about the same population size but companies in Europe have not become as large as their US counterparts. In terms of market capitalization, only one EU company

(LVMH Moet Hennessy, France) is included in the world’s top twenty companies, a list dominated by companies from the US and Asia.22 In terms of sectors, four of the top five companies are US tech firms (Apple, Microsoft, Alphabet and Amazon). The list of top fifty companies by market capitalization includes only a few businesses in EU countries.

The gap in the valuation of companies in the EU compared to its trading partners is a cause for concern. Explanations for this development are wide and varied. EU countries cannot directly control population aging and rising demands on public spending in welfare states. But developments highlight the importance of structural issues that EU countries can control, such as the regulatory framework for businesses. In the next section, we discuss and compare the effects of regulation between EU countries and their trading partners.

All countries regulate businesses, ranging from requirements to start the business to the payment of taxes and the fulfillment of fiduciary duties.

We can think of this kind of regulation as general, because it applies to all firms, whether they are domestic or foreign service providers. But even when regulations apply to all, they tend to be more burdensome to non-domestic businesses. There are several reasons for this. For one, language and culture present obstacles. Information about requirements might not be available in other languages. Though the European Commission provides an information site to serve as ‘a single point of contact’, in practice information in other languages tends to be fragmented and sites are easier to navigate for domestic users.

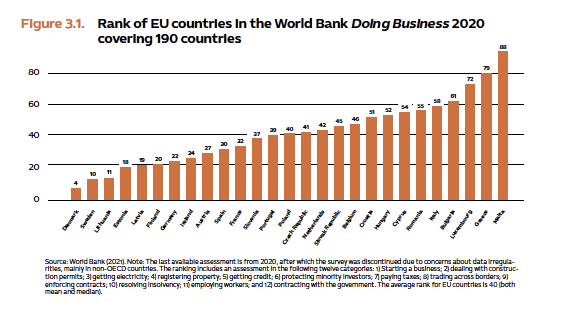

Until 2021, overall hurdles that affect all businesses were collected by the World Bank and published in its Doing Business Report. The report has since been discontinued, but the last available publication provides some general information about red tape for businesses in twelve categories. Figure 3.1 lists the EU countries that are included in the 2021 publication. It is noteworthy that only six EU MS made the top twenty ranking, and only ten were included among the top 30 out of 190 countries. Nine EU countries were ranked below 50 in the world (in Figure 3.1, Croatia and countries to its right).

The OECD launched the Services Trade Restrictiveness Index (STRI) in 2014. The publication of the index is an annual exercise where trade restrictions in services are assessed and updated by trade experts, resulting in an index that has a value of zero for no restrictions and one for a completely closed economy.23 There are 22 sectors in the index and it covers fifty economies, including the OECD countries.

In this section, we analyze a subset within the OECD STRI database that focuses on intra-EEA trade in services only. In general, the intra-EEA measure is an order of magnitude lower than those that include the full set of countries.

Service trade restrictions by country

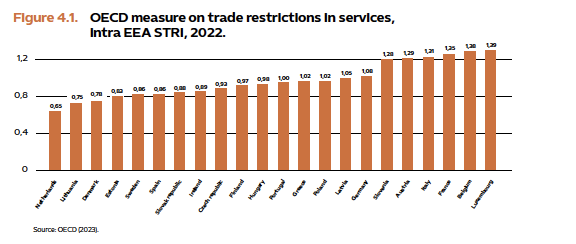

The STRI database is comprehensive, and it is helpful to summarize the data in easily discernable dimensions. We will consider three ways to extract information from the STRI database to better understand service trade restrictions across EU countries. The first, and most straightforward way, is to list countries according to their total intra-EEA STRI score, obtained by summing all the sectors per country (see Figure 4.1).25 According to the intra-EEA, the Netherlands has the least number of restrictions and Luxembourg the most within the EU single market.

With the inclusion of Portugal and Spain in the set of countries with few restrictions, it is worth underlining that the distribution of trade obstacles (as measured by the intra-EEA STRI) only partially represents the ‘frugal’ north.

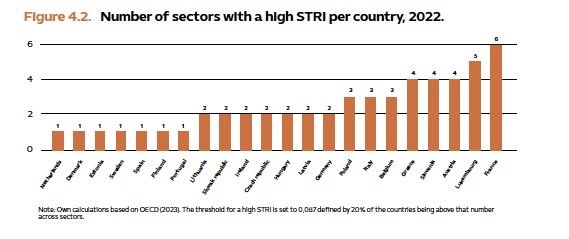

Secondly, we can aggregate the information to determine how many times a country has a sector that is above some threshold. This is done in Figure 4.2. The threshold is computed as the level of the intra-EEA STRI that represents the top quintile of countries (i.e. the twenty percent of MS with the highest trade obstacles in the intra-EEA STRI). In this way, it is clear that there is a group of countries with consistently low barriers to trade in services, notably the Netherlands, Denmark, Estonia, Sweden, Spain, Finland and Portugal; conversely, the countries with consistently high barriers to trade in services are France, Luxembourg and Austria. With the inclusion of Portugal and Spain in the set of countries with few restrictions, it is worth underlining that the distribution of trade obstacles (as measured by the intra-EEA STRI) only partially represents the ‘frugal’ north.

A third way to extract information on the distribution of trade obstacles is to count the number of times a country has the highest intra-EEA STRI score for a given sector. In Table 4.1, we can see that this list to a large extent overlaps with the countries in Figure 4.2 that exhibit relatively high trade obstacles. One difference is that Slovenia now has the top position instead of France. How can we understand these different ways to view obstacles to trade in services? Figure 4.2 captures countries that belong to different groups in terms of trade restrictiveness, whereas Table 4.1 picks out those countries that are the most extreme in a particular sector.

Table 4.1. EU countries with the highest trade restrictions in selected service sectors

| Country | No | Sectors |

|---|---|---|

| Slovenia | 5 | Insurance, logistics cargo hand- ling, logistics storage and ware- house, maritime transport, and motion pictures |

| Belgium | 4 | Architecture, courier services, logistics customs brokerage, and telecommunications |

| Luxembourg | 3 | Accounting, construction and engineering services |

| Italy | 2 | Broadcasting and sound recording |

Trade restrictions according to sector

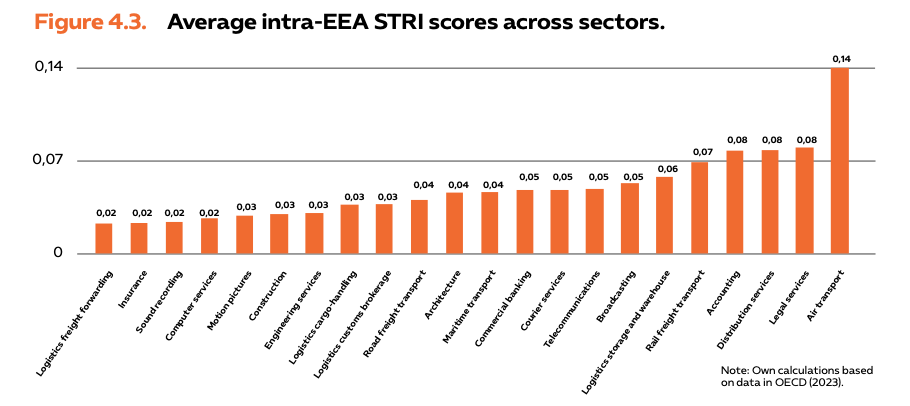

There are considerable differences in the number of restrictions across sectors. As can be seen from Figure 4.3, the area with the most restrictions in the intra-EEA STRI is Air transport. It is exempted from the EU service sector agreement (EU 2006) and has its own rules and regulations. The area with the lowest trade restrictions is Logistics freight forwarding.

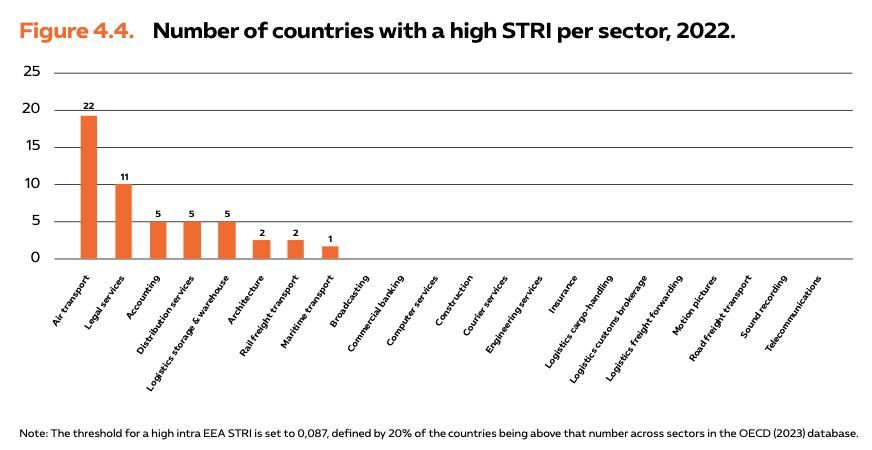

As can be seen in Figure 4.4, air transport, legal services, accounting and distribution services are especially prone to regulatory hurdles. In the figure, we calculate the number of times a country is above a certain threshold, using the same threshold as in Figure 4.2, i.e. the point above which 20 percent of countries are above that number across sectors.

Conversely, we can ask the reverse question and find which sectors have low intra-EEA STRI measures across EU countries, as shown in Table 4.1.

Table 4.1. Sectors with low levels of intra EEA STRI restrictions across EU, 2022.

| Sectors with few restrictions | Sectors with medium restrictions |

|---|---|

| Logistics freight forwarding, insurance, sound recording, computer services, motion pictures, construction and engineering services | Logistics cargo-handling, logistics customs brokerage, road freight transport, architecture, maritime transport, commercial banking |

Given all this information about regulatory hurdles and obstacles, which areas should be at the top of the list for regulatory reform?

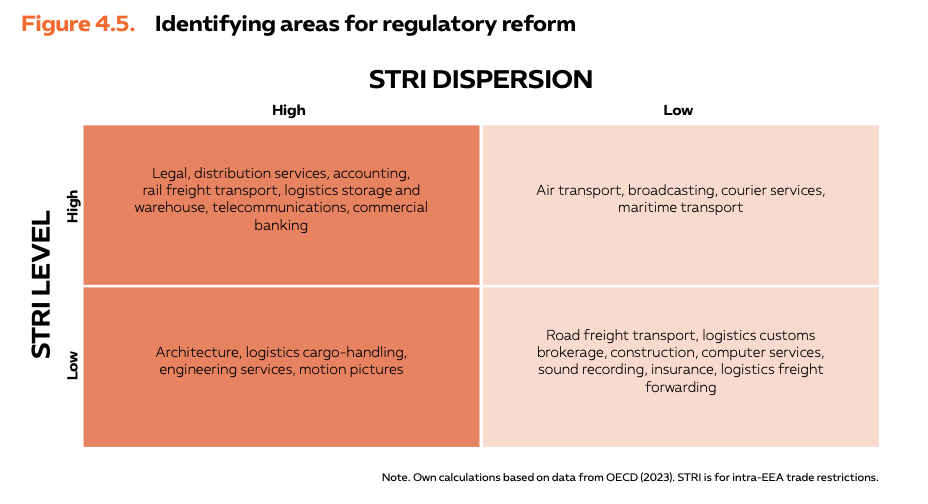

One way to think about this issue is to consider the level of trade obstacles together with their dispersion across countries (i.e. the variance).

Using these measures, we can use benchmarking for sectors and countries. For simplicity, we sort the countries according to the size of their intra- EEA STRI and divide them into two groups, one below and one above the median country. We do the same for the variance.

This results in four sets of sectors:

- Sectors with both a high intra-EEA STRI and variance;

- Sectors with a high intra-EEA STRI but low variance;

- Sectors with a low STRI but high variance;

- And sectors with both a low intra-EEA STRI and a low variance.

Areas to the right in Figure 4.5 (with white background) are arguably less ripe for reform.

Or at the very least, these sectors should not be on the top of a reform agenda. With a low level of trade obstacles as well as small differences between countries (the lower right- hand quadrant), the conditions for competition from other EU countries are already relatively favourable. Turning next to the situation with high trade obstacles and low dispersion (the top right-hand quadrant), an argument can be made for the ‘public interest’ perspective to override competition concerns. By contrast, a case can be made for regulatory reforms for those sectors on the left-hand side of Figure 4.5. When both the dispersion and the level of obstacles are high, this indicates that EU countries make heterogenous assessments. Countries with high intra-EEA STRI in legal distribution services, etc. would do well to re-assess, asking if the original motivations for these restrictions still hold, and whether they reflect the public interest or merely the successful influence peddling of special interest groups. Finally, the same argument can be made for those sectors with high dispersion but low average levels of restrictions (the lower left-hand quadrant). For these sectors, some countries stand out because of their high restrictions, for example, Belgium’s restrictions on architectural services and Slovenia’s on logistics cargo handling (see also Table 4.1 above).

…whether they reflect the public interest or merely the successful influence peddling of special interest groups.

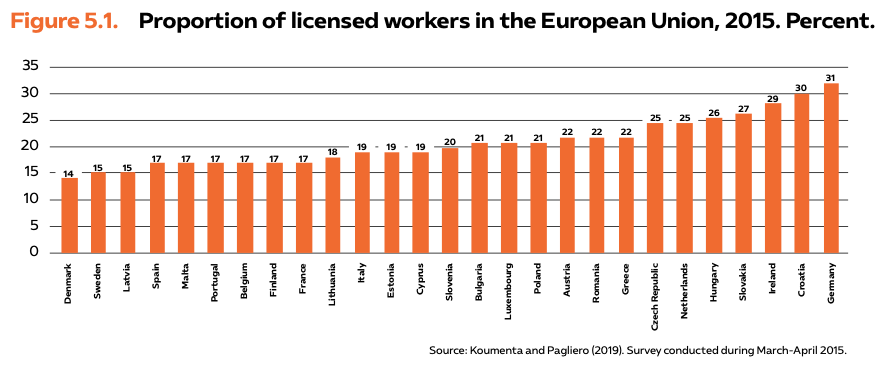

The 2015 survey on regulated professions

A 2015 survey examining 6,690 regulated professions in the EU showed that occupational regulation affects about 22 percent of workers in the European Union.27 In the aggregate, licensing of workers is associated with a wage premium of about 4 percent and larger wage inequalities within sectors. Also, employment levels are estimated to be about 3–9 percent lower as a result of licensing.

The survey revealed large disparities between EU countries. Denmark, the country with the lowest proportion, requires licensing for 14 percent of jobs, while Germany is at the other end of the spectrum with 33 percent (see Figure 5.1).

Behind the aggregate values in Figure 5.1, there are some notable sector differences. In 2015, Germany had the highest number of restrictions in the EU in three areas (manufacturing products, finance & real estate and public administration); Croatia had the highest number of restrictions in three areas (health & social work, professional services and culture activities). At the other end of the spectrum, Luxembourg had the fewest restrictions in three areas (agriculture, manufacturing products and finance & real estate).

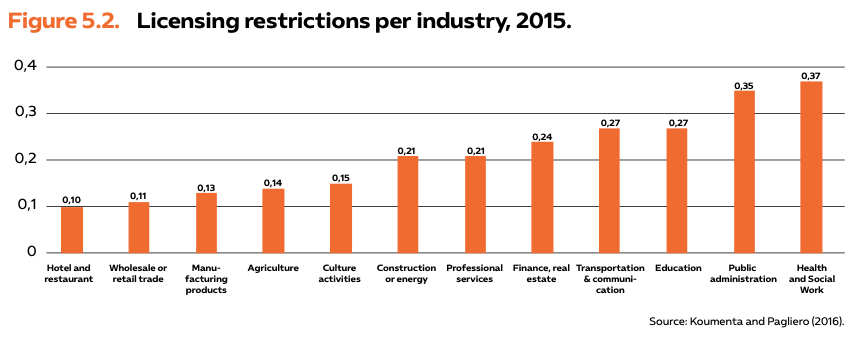

We can also analyse the differences between sectors based on the 2015 survey data. These tend to be somewhat larger than the differences between countries. It can be seen from Figure 5.2 that the sector with the least restrictions is hotel & restaurant services, and the area with the most restrictions is health & social work. This is not surprising, as health and social work involve the medical professions and other sensitive jobs that have been accorded special exemptions in the EU Service Directive.

For a few select professions, the EU has introduced the European Professional Card (EPC). By applying for the card, workers can receive a qualification that may be recognized by other EU countries. For now, however, the EPC it is limited to a small selection of professions: mountain guide, nurse, pharmacist, physiotherapist and real estate agent.28

The EU Points of Single Contactportal’s uneven quality

To help individuals and businesses export within the Single Market, the European Commission has introduced the Points of Single Contact portal.29 It collects links to each country’s PSC website in the EU and EEA, thereby centralizing information. While the service is helpful, the quality of the different country websites is uneven. In many instances, the information is hard to access and navigate (see Table 5.1).

The European Commission’s Points of Single Contact portal leads to country websites of uneven quality.

Points of single contact on restricted professions.

| Country | Other languages | Quality of information content | Examples of restricted/ sensitive professions |

|---|---|---|---|

| Austria | English but not complete | Fairly complete, but requirements may differ depending on region. Some information only available in German. One regional web sites do not load (Carinthia, 1/1/2023) | Baker, foot care, forest assistant, mountain guide, chimney sweep, repair of motor vehicles |

| Belgium | English, French, German and Dutch | Information on restricted professions only provided in French in an awkward table | Baker, real estate agent, mountain guide |

| Bulgaria | English | Have to choose one of 28 regions and then muncipality, information is then ru- dimentary and some not accessable | After clicking on information for temporary construction work, information only provided in Bulgarian |

| Croatia | English, but most detail is in Croatian | Overview good, but site lacks specific information in English | Driving schools, tourism |

| Cyprus | English | Fairly easy to access | Real estate, tax consultant, caterer, Swimming pool operator |

| Czech Republic | English but fragmented | Information difficult to access and refers to specific sites for different municipalities | Information not in English |

| Denmark | English | Provides overall information but hard to access specific professions | Cook, steward at sports events |

| Estonia | English but limited information | Web site leads to information primarily related to social security, pensions, car ownership etc | Search for restricted professions lands in awkward information list |

| Finland | English | Simple and clear structure | Chimney sweep, refrigirator fitter, secu- rity guard |

| France | English but awkward website | Web site easy to navigate but partially malfunctioning | Baker, confectioner-ice cream parlour, mountain guide |

| Germany | Limited in English, some Polish | Requires to click on each region. Four regions have links that lead to empty or unused web sites 1/1/23 (Schleswig Holstein, Rheineland-Palatinate, Saarland, Baden-Württemberg) | Baker, Call center, perfume worker |

| Greece | English | Information is fragmented and awkward | Sports operator, diving instructor. Search function requires a minimum of 5 charac- ters and so excludes for example cook |

| Hungary | English | Provides an easy to read excel file with restrictred professions and which is the relevant authority | Driving instructor, machine operator, sculptor, shoemaker |

| Ireland | English, French, Polish, Italian, Spanish and German | Information easily summarized but de- tails are unavailable in other languages | Crane operator, driving instructor, restaurant, tourist guide |

| Italy | English | Information on restricted professions is easy to access and links are provided to relevant authorities | Mountain guide, hairdresser, real estate agent, pest control, driving instructor, fencing master, ski instructor |

| Latvia | English | Accessible but lacking information | Clicking on professions leads to a non-informative search site |

| Lithuania | English | Web site does not list regulated professions and instead refers back to the European Commission’s web page | Lists some medical and veterinary professions |

| Luxembourg | French, German and English | Website gives overview of requirements on businesses but lacks specifics | Hard to find |

| Malta | English | Website gives overview of requirements on businesses but lacks specifics | Hard to find |

| Netherlands | English | Website gives overview of requirements on businesses but lacks specifics | Hard to find |

| Poland | English | Website gives overview of requirements on businesses but lacks specifics | List of regulated professions is in Polish |

| Portugal | English | Overview only | Hard to find |

| Romania | – | No overview | No information |

| Slovakia | English | Rudimentary website but provides information on professions | Brewer, driving school instructor, tour operator, testing of chimneys |

| Slovenia | English | Rudimentary website but provides information on professions | Cave guide, librarian, fisherman, ships cook |

| Spain | Basque, Catalan, Galic and English | Minimalist information and links that lead to error messages (for English version) | Hard to find |

| Sweden | English | Simple overview and easy to navigate | Diving work, mountain guide, Real estate agent |

The following issues emerge:

- Not all information is available in English.

- Each domestic site has a different structure and logic.

- Some also provide information on social security and non-business-related governmental services.

- For some federal MS (such as Germany and the Czech Republic), the user first must select a region and then a municipality.

- It is unclear how current the information is and how often it is updated

The current vintage of regulated professions in the EU can be accessed through another EU webpage.30 This allows the user to search for a specific profession and determine the current regulatory requirements in the country of interest as well as what qualifications are needed. For example, searching for ‘cook’ yields a list of 10 EU countries where there are various forms of accreditation requirements; for driving instructor, there are 21 countries; for chimney sweep, there are 10.31

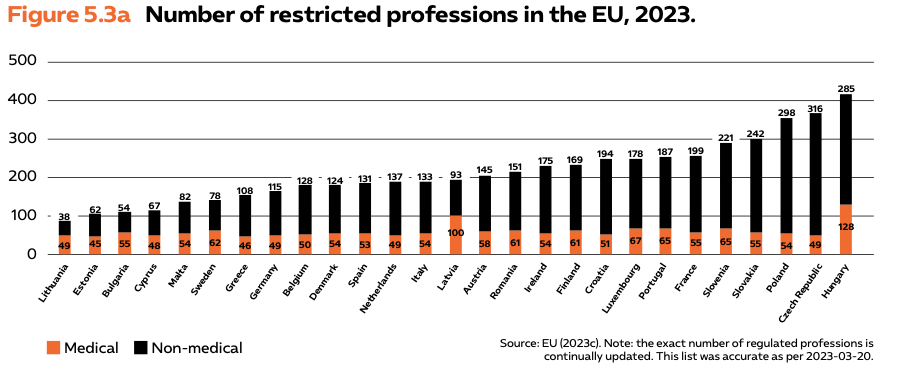

In the European Commission’s database for 2023, there are 5,701 regulated professions in total for the 27 MS, about 15 percent lower than the 2015 tally of 6,690. All countries regulate medical professions, such as doctors, veterinaries and nurses, which are specifically exempted in the Service Directive. Of the restricted professions, most are non-medical, but the proportion differs across countries (see Figure 5.3a). In 2023, there is a total of about 4,110 professions not related to the medical professions. Most countries have about 60 regulated medical professions; in Latvia and Hungary, the proportion is higher. Overall, most differences in regulation of services across the EU are explained by the number of regulated non-medical professions.

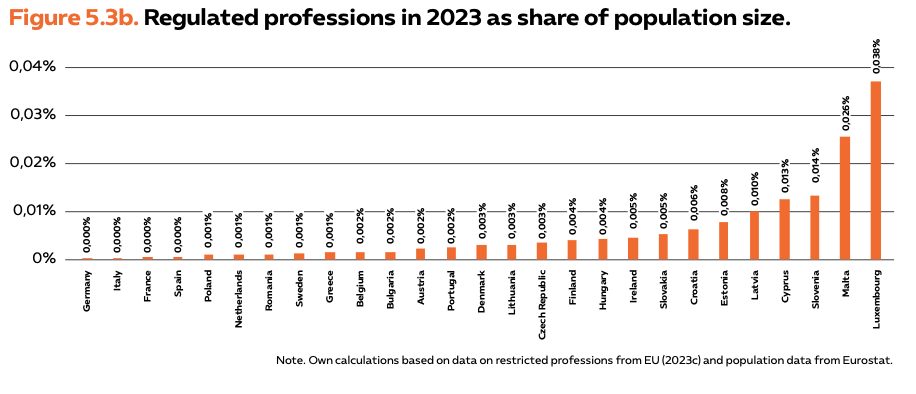

This list of regulated professions does not incorporate other information about the labour market and does not account for possible effects from population size. In large countries, the labour market may contain more types of professions and services than that of a small economy. Therefore, comparing regulated professions to population size provides crucial information. For example, if a small country has a large number of regulated professions, these will be more dominant in the labour market, and arguably a more problematic feature of the economy.

In Figure 5.3b, we can see that the order of countries changes compared to Figure 5.3a. Large economies (Germany, Italy, France and Spain) have the lowest number of regulated professions adjusted for population size. By contrast, Luxembourg appears at the opposite end of the spectrum, with many regulated professions relative to its population size. Arguably, the most useful way to read the diagram is not to ‘excuse’ large countries for having little regulation compared to their economy, but to highlight the small economies that should have fewer regulated professions.

Arguably, the most useful way to read the diagram is not to ‘excuse’ large countries for having little regulation compared to their economy, but to highlight the small economies that should have fewer regulated professions.

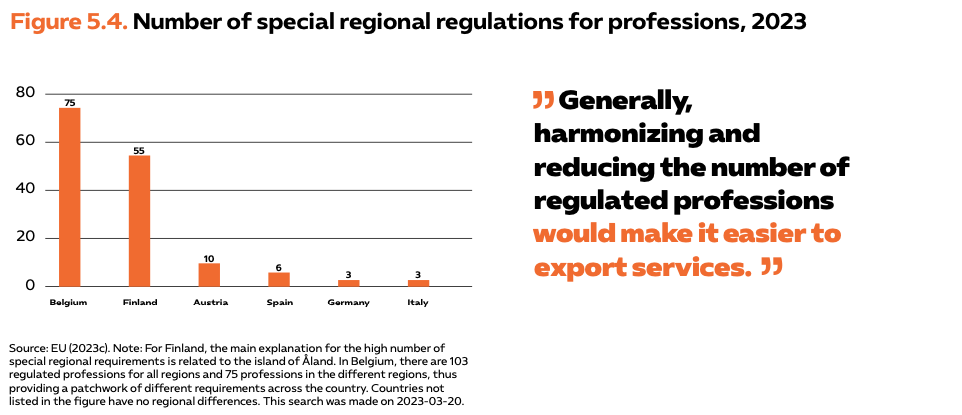

Some countries have different requirements for professions within the country, where some regions impose provisions that do not exist elsewhere. In 2023, 152 out of 5,438 professions had regional idiosyncrasies. Belgium stands out in this regard, with a fairly large number of regional differences (see Figure 5.4). For example, in the region of Wallonne, there is a special requirement on ‘light vehicle standards officer’. In the Italian region of Lazio, there are special requirements concerning tattooing and body piercing.32 Notably, Germany has only three professions that have different requirements despite granting its regions considerable autonomy. Two of these restrictions stem from the region of Bayern, which imposes special conditions on mountain and ski guides and on ski instructors.

Having different requirements inside the country results in an additional layer of complexity and hinders the free movement of labour. Given that most countries do not have special requirements within the country, those that Figure 5.4 highlights should consider reducing – or eliminating the within-country differences. Generally, harmonizing and reducing the number of regulated professions would make it easier to export services.

Towards fewer regulated proffessions

As noted in the previous section, in 2023 there are about 5,700 regulated professions in the EU obtained by summing the value for all countries (displayed in Figure 5.3a). The smallest number of regulated professions is in Lithuania (87) and the greatest is in Hungary (413). Each country makes its own determinations about when and why a profession should be regulated. This hampers competition and the free movement of labour in various ways. The European Commission has published a methodology that pinpoints the sources of ineffective competition related to several dimensions, including issues related to information asymmetries and service differentiation.33

It is unreasonable to view the total 5,700 as being a fair representation of the total number of regulated professions. Summing regulated professions across the EU ignores the fact that there will be a large amount of overlap. For example, requirements to become a driving school instructor cannot reasonably differ all that much in EU countries. For some professions, the requirements may be almost identical. In practice, this implies that the number of distinct regulated professions in the EU ought to be a lower number than 5,700.

This issue is important for at least two reasons. First, when regulatory idiosyncrasies are reduced and regulations harmonized across the EU, this facilitates the movement of labour. Indeed, research on regulated professions in the EU has shown that there is a robust positive relationship between recognition of qualifications and trade in services.34 Second, reducing the regulatory burden is associated with lower costs of administration, both for governmental agencies and for firms.

One challenge is selecting the best criteria for identifying regulated professions that could be harmonized or deregulated. Another, more mundane challenge is that each profession is specified in the original language of the country in the EU database. While the database of regulated professions contains translations to English, the information is cumbersome to access as well as time-consuming. Moreover, the English translation does not have an ’official’ status.

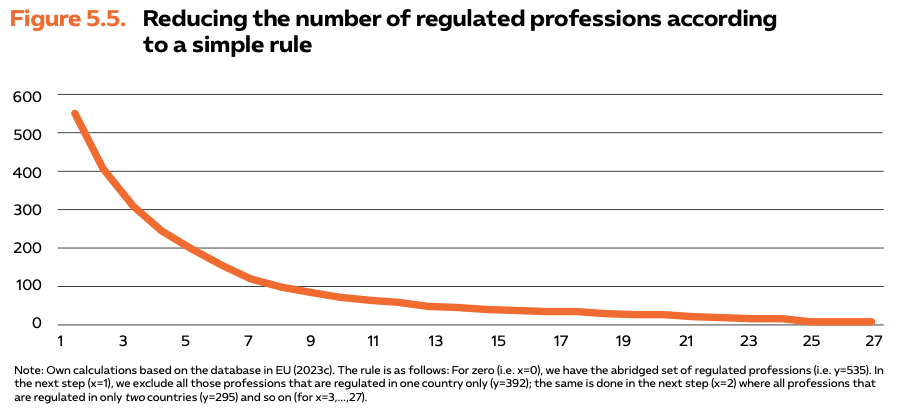

However, the English translation of each profession is still a useful starting point for creating a shorter list. This is not difficult; one way to do it is as follows. We used the English translation of each profession to make a list of regulated professions that contains the entries for all EU countries. This exercise is simple and results in a massive reduction in the number of professions, from about 5,700 to 535, as the aggregate number contains numerous duplicates of the same profession. This lower number is still above the maximum value of 413 in Hungary, but represents all professions in the EU.

It is possible to reduce this number of regulated professions even further. If many, or all countries, restrict some profession (such as medical doctor) this is a strong argument for the ‘public interest’ argument. But the converse also holds. If only one country regulates a certain profession, or only a few do, then the ‘public interest’ argument is weak. Perhaps the profession in question should not be regulated at all.

The starting point for the computation is the abridged list of 535 regulated professions. For the first step, we sum all countries that are alone in regulating a given profession. Table 5.1 lists examples of professions that are regulated in only one country.

Table 5.1. Examples of professions regulated in one country only.

| Accounting technician – Ireland | Agronomist-technician – Portugal |

| Arts therapist in the health service – Austria | Barrelmaker – Slovenia |

| Crane technician – Poland | Engraver – Luxembourg |

| Florist – Luxembourg | Itinerant trader – Italy |

| Kennel manager – Netherlands | Manufacture of cosmetic products – Sweden |

| Mountain sport instructor – France | Owner of a dance school – Austria |

| Sculptor – Luxembourg | Shipbuilding – Germany |

| Tailor (ladies/men’s)/Dressmaker – Croatia | Wine taster – Slovenia |

This thought experiment can be extended to illustrate one way to prune the number of regulated professions. More specifically, the same qualitative argument can be made for questioning the wisdom of professions that are regulated in only two countries, three countries and so on. This is done in Figure 5.5. In each step, the number of countries needed to exclude a profession increases. For example, after 6 steps, 111 regulated professions remain. Indeed, initially the reduction is quite rapid.

How can this thought experiment be used? The method is illustrative but makes explicit the issue: when only a few countries regulate a profession, a good case can be made that the profession should be subject to liberalisation or harmonisation. For example, questioning all professions that are regulated in only two countries, but not in the remaining EU countries, yields a 45 percent reduction in the number of regulated professions, thus benefitting the free movement of labour and reducing administrative costs. Table 5.1 would be a good start for reviewing what professions should be deregulated.

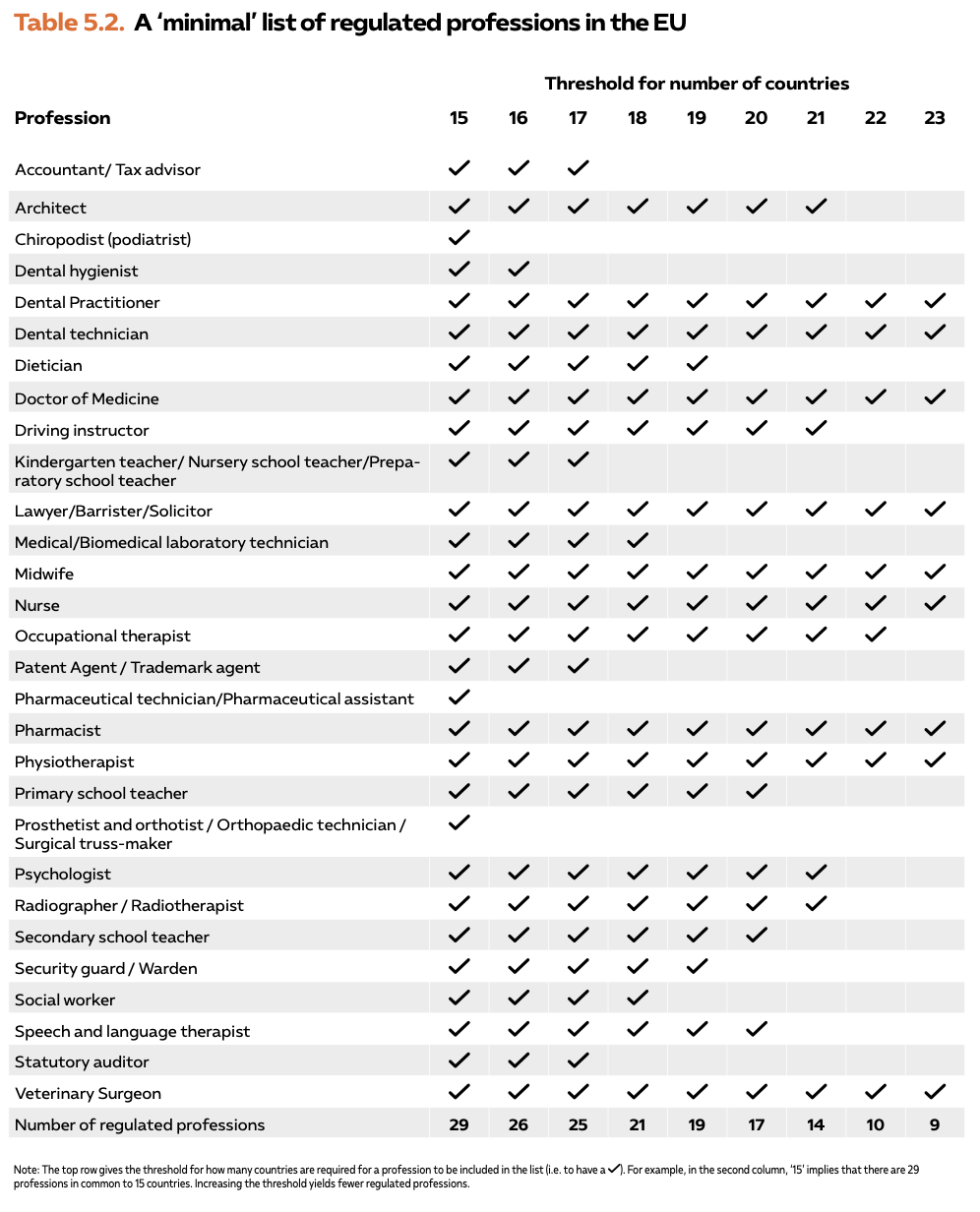

This thought experiment can be extended further. Suppose we specify a threshold for how many countries need to be included to make a ‘common’ list of regulated professions in the EU. By increasing the threshold, the number of professions included becomes successively smaller (see Table 5.2). For example, if we require that a profession should be regulated in 23 EU countries, this yields a rather minimalist list of 9 professions, compared to the thousands in the EU database. This should not be seen as a precision exercise but rather an illustration of how some effort toward simplification and consolidation could yield a much shorter list of regulated professions. The table can also be used to show which threshold results in inclusion or exclusion for a specific profession. For example, kindergarten teachers are regulated in 17 countries and unregulated in 10. The medical professions are regulated in all 27 EU countries.

The table can also be used to show which threshold results in inclusion or exclusion for a specific profession. For example, kindergarten teachers are regulated in 17 countries and unregulated in 10.

Services are heterogenous and each sector is different; correspondingly, skills requirements vary greatly. This puts the service sectors at a disadvantage, both in terms of harmonization and scalability.

Some regulatory hurdles get political attention, but many do not. Even when an obstacle may be large in a given sector, it may be small from a regulatory standpoint, in the larger scheme of things. Unless a question is considered sufficiently ‘big’, it may be hard to escalate up the political ladder to achieve action. Notably, a European Commission study sampled several sectors and identified more than 50 obstacles to the Single Market, ranging from regulation of accounting and tax advice to waste management (see Table 6.1).35 In waste management, for example, one issue is “non-harmonized end- of-waste criteria.”36

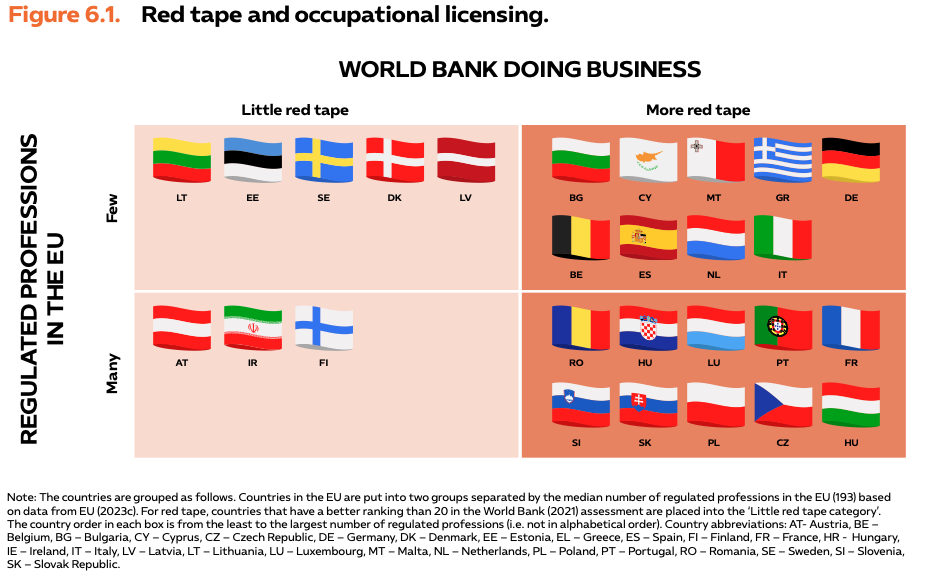

It is useful to put these many minor obstacles into an overall macro context. One way to do this is by combining different types of rankings of red tape and bureaucracy. More specifically, in Figure 6.1 the list of occupational licensing for professions is combined with the ranking of countries in the World Bank Doing Business assessment. A brief explanation is as follows. The EU occupational licensing requirements are divided into two groups: one with the number of regulated professions below the median and one above the median; for Doing Business, countries are divided into those that are below the rank of 20 and those that are above.

What happens when we combine rankings of regulated professions, the red tape measure from the World Bank and the OECD STRI index? Not all EU countries are in the OECD, but it is still informative in giving a list of those countries that manage to curtail bureaucracy in several dimensions: Denmark, Estonia, Lithuania, Spain and Sweden. From the top-left quadrant in Figure 6.1, this list excludes Latvia because it has a mediocre score in the OECD STRI.

The countries that consistently suppress bureaucracy are Denmark, Estonia, Lithuania and Sweden.

Finally, let us combine the measure of bureaucracy from the World Bank with the size of each market in terms of GDP. It turns out that countries ranked highly in the World Bank’s bureaucracy assessment represent a relatively small share of EU GDP (see Figure 6.2). The EU countries with a top twenty ranking in the survey (Denmark, Sweden, Lithuania, Estonia, Latvia and Finland) account for less than 9 percent of EU GDP. Large EU countries, such as France and Germany, are ranked 32 and 22, respectively; Italy is ranked 58. EU countries with a lower rank than 20 in the World Bank assessment together represent about 90 percent of EU GDP. As such, there is considerable scope for deregulation in substantial portions of the EU.

EU coutries with a lower rank than 20 in the World Bank assessment together represent about 90 percent of EU GDP. As such, there is considerable scope for deregulation in substantial portions of the EU.

Trade in services tends to be more complex to regulate than trade in goods, but this does not mean we should abstain from reforms. Intra-EU trade in services is at the same level as extra-EU trade in services, when measured as a share of GDP— a sign that much more needs to be done. Reductions in red tape and trade obstacles will increase employment and benefit both consumers and firms. The peer pressure mechanism in the EU needs to be more vital to yield improvements or substantial reforms. And it is time to put service trade liberalization high on the reform agenda.

After almost three decades with a Single Market that has not substantially grown trade in services, the EU should consider the following set of reforms:

- The list of EU-regulated professions should be regularly pruned and harmonised;

- A comprehensive review should examine most sectors for areas that could be liberalized.

- Enforcement should shift from soft compliance mechanisms to legally binding rules.

The lack of service sector reforms has consequences for competitiveness in the EU. A vibrant service sector supports the whole economy, including industry and manufacturing. Over many years, companies in the US and Asia have grown faster in terms of market capitalization. US tech companies dominate the absolute top.

There are many structural issues outside the direct control of governments, but regulation is not one of them. Without a comprehensive overhaul of regulation in the EU, competitiveness may further erode.